How to Stop Impulse Buying and Save Money [Budgeting Tips]

Understanding the Concept of Triggers

Triggers are like invisible puppeteers—they pull the strings of our emotions and actions without us even realizing it. Spotting these hidden influencers is the cornerstone of regaining control over your spending habits. When you understand what sets off your impulses, you can craft personalized defenses against them.

The goal isn't to live in a trigger-free bubble, but to develop awareness of how these catalysts shape your financial decisions. Imagine walking through a minefield with a map—that's what trigger recognition gives you in the world of impulse spending.

Types of Triggers: Emotional and Behavioral

Triggers come in different flavors, each with its unique impact. Emotional triggers might include nostalgic commercials that make you yearn for childhood treats, or stressful days that send you straight to online shopping for comfort. These emotional landmines can detonate without warning, leaving your budget in shambles.

Behavioral triggers operate like conditioned responses. That mid-afternoon break where you automatically browse sale emails, or the habitual checkout lane candy grab—these are behavioral patterns masquerading as harmless routines.

Environmental Triggers: Places and People

Your surroundings can be a minefield of temptation. That particular aisle in Target where you always find irresistible home decor, or the mall food court that triggers unnecessary snack purchases—these locations become danger zones for your wallet.

Social influences wield surprising power too. Shopping with a friend who always encourages treat yourself purchases, or following influencers who constantly showcase new products can turn discretionary spending into a reflex.

Cognitive Triggers: Thoughts and Beliefs

Mental shortcuts like I deserve this or It's on sale so I'm saving money can override rational decision-making. These thought patterns often stem from deeper beliefs about money, self-worth, or scarcity.

Unraveling these mental knots is like giving yourself x-ray vision into your spending psychology. When you recognize that retail therapy is actually emotional first aid, you can find healthier alternatives.

Physical Triggers: Sensations and Illnesses

Don't underestimate physical states. Hunger can make everything in the grocery store look appealing, while fatigue lowers your resistance to impulse buys. Even something as simple as caffeine can amplify spending urges by increasing impulsivity.

Trigger Avoidance vs. Management

Complete avoidance is neither practical nor desirable—after all, you can't live your life avoiding stores or the internet. The real power lies in developing what psychologists call response prevention—the ability to acknowledge triggers without automatically reacting to them. Techniques like the 24-hour rule (waiting a day before purchasing) can short-circuit impulsive responses.

The Importance of Self-Reflection

Building trigger awareness is like detective work on yourself. Review your bank statements looking for patterns—are most impulse buys in the evening? After stressful meetings? When you're bored?

Keeping a spending mood journal can reveal surprising connections between your emotional state and purchasing decisions that you'd never notice otherwise. This isn't about judgment—it's about gathering intelligence on your personal spending tendencies.

Building an Emergency Fund: Preventing Financial Crises and Reducing Stress

Establishing a Realistic Savings Goal

Begin by calculating your survival number—the bare minimum needed to cover essentials for one month. This includes just four walls: housing, utilities, basic groceries, and transportation. Everything else is negotiable in a true emergency. This stripped-down approach helps create an achievable first target.

While conventional wisdom suggests three to six months of expenses, consider building in tiers—a $1,000 starter emergency fund for immediate crises, then gradually working toward larger buffers. This phased approach makes the goal feel less overwhelming while still providing meaningful protection.

Developing a Savings Plan

Turn saving into a game by using the round up method—every transaction gets rounded up to the nearest dollar (or five dollars) with the difference going to savings. These micro-savings add up surprisingly fast without feeling painful.

Another clever strategy: Create a snowflake savings system where unexpected money (rebates, gift cards, found cash) automatically gets converted into emergency fund contributions. It's like financial alchemy—turning small windfalls into security.

Prioritizing and Automating Savings

The secret weapon of successful savers? Paying yourself first—literally. Set up a separate savings account at a different bank from your checking, making it just inconvenient enough to access that you'll think twice before dipping in. Automate transfers to happen right after payday, so the money disappears before you can spend it.

Behavioral economics shows we're more likely to save when it's the path of least resistance. That's why automation works—it removes the need for willpower in the moment.

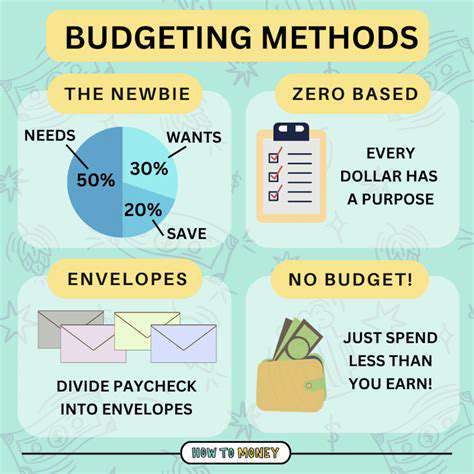

Budgeting and Tracking Progress

Ditch traditional budgets for a values alignment approach. Instead of rigid categories, ask: Does this spending move me toward my emergency fund goal? This mindset shift transforms saving from deprivation to empowerment.

Visual trackers can provide powerful motivation—whether it's coloring in a savings thermometer or moving marbles from one jar to another. Our brains respond powerfully to visible progress markers.

Maintaining and Adapting Your Strategy

Treat your emergency fund like a living thing—it needs regular check-ups. Schedule quarterly financial physicals where you review your fund's size relative to current life circumstances. A new job with less stability? Maybe boost your target. Paid off significant debt? You might adjust downward.

The most resilient emergency funds evolve with your life. They're not static numbers but dynamic safety nets that flex as your risks and responsibilities change over time.

Read more about How to Stop Impulse Buying and Save Money [Budgeting Tips]

![Best Investment Strategies for Volatile Markets [2025]](/static/images/30/2025-05/StrategicAssetAllocation3AAdaptingtoMarketConditions.jpg)

Hot Recommendations

- How to Budget for Home Renovations

- Understanding Estate Taxes

- How to Dispute Errors on Your Credit Report

- How to Pay Off Credit Card Debt with Zero Interest Offers

- Understanding Algorithmic Trading (Basics)

- How to Save Money on Entertainment

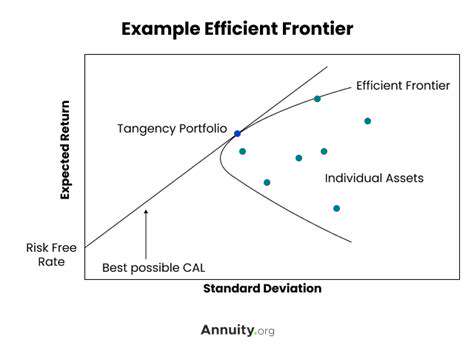

- Understanding the Efficient Frontier in Portfolio Building

- Tips for Improving Your Credit Utilization Ratio

- Guide to Investing in Global Markets

- Saving Money Tips for Paying Off Debt Faster